Industrial Minerals proposes to revise all Shanxi-origin bauxite specifications at the end of October.

from MPW - Pricing News http://ift.tt/2dL6Mcn

via IFTTT

Friday 30 September 2016

Personal Income increased 0.2% in August, Spending increased less than 0.1%

The BEA released the Personal Income and Outlays report for August:

The following graph shows real Personal Consumption Expenditures (PCE) through August 2016 (2009 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.

The dashed red lines are the quarterly levels for real PCE.

The increase in personal income was at consensus expectations. And the increase in PCE was below the 0.2% increase consensus.

Using the two-month method to estimate Q3 PCE growth, PCE was increasing at a 3.1% annual rate in Q3 2016. (using the mid-month method, PCE was increasing 2.6%). This suggests decent PCE growth in Q3, even with the weak August report.

from Calculated Risk http://ift.tt/2dEX3RY

via YQ Matrix

Personal income increased $39.3 billion (0.2 percent) in August according to estimates released today by the Bureau of Economic Analysis. ... personal consumption expenditures (PCE) increased $6.2 billion (less than 0.1 percent).The August PCE price index increased 1.0 percent year-over-year and the August PCE price index, excluding food and energy, increased 1.7 percent year-over-year.

...

Real PCE decreased 0.1 percent. The PCE price index increased 0.1 percent. Excluding food and energy, the PCE price index increased 0.2 percent.

The following graph shows real Personal Consumption Expenditures (PCE) through August 2016 (2009 dollars). Note that the y-axis doesn't start at zero to better show the change.

The dashed red lines are the quarterly levels for real PCE.

The increase in personal income was at consensus expectations. And the increase in PCE was below the 0.2% increase consensus.

Using the two-month method to estimate Q3 PCE growth, PCE was increasing at a 3.1% annual rate in Q3 2016. (using the mid-month method, PCE was increasing 2.6%). This suggests decent PCE growth in Q3, even with the weak August report.

from Calculated Risk http://ift.tt/2dEX3RY

via YQ Matrix

Price Briefing 23-29 September

Most industrial minerals' spot prices remained unchanged week-on-week as the Chinese market shut ahead of the Golden Week national holiday. Ongoing weak demand for steel and cement pulled metspar prices down.

from MPW - Pricing News http://ift.tt/2df9c1L

via IFTTT

from MPW - Pricing News http://ift.tt/2df9c1L

via IFTTT

Thursday 29 September 2016

Friday: Personal Income, Chicago PMI, Consumer Sentiment

From Merrill Lynch: Elections: what keeps us up at night?

Friday:

• At 8:30 AM ET, Personal Income and Outlays for August. The consensus is for a 0.2% increase in personal income, and for a 0.2% increase in personal spending. And for the Core PCE price index to increase 0.2%.

• At 9:45 AM, Chicago Purchasing Managers Index for September. The consensus is for a reading of 52.0, up from 51.5 in August.

• At 10:00 AM, University of Michigan's Consumer sentiment index (final for September). The consensus is for a reading of 90.1, up from the preliminary reading 89.8.

from Calculated Risk http://ift.tt/2cZUJ6W

via YQ Matrix

The US elections are quickly approaching and, in our view, have become one of the most significant near-term risks for the economy and markets. The facts are changing quickly, both in terms of the policies that each candidate supports but also in terms of expectations over the outcome of the election. According to the Iowa Electronic Markets (IEM) and PredictWise, Clinton currently has about a 70-75% chance of winning the election. FiveThirtyEight, a political aggregator, is expecting a closer race with Clinton’s chances at only about 60%. According to IEM and PredictWise, the probability of Republicans retaining control of the House is running at 70%-90%, and the probability of Democrats taking control of the Senate is about 40%-60%.CR Note: All key analysts are assuming Ms. Clinton will be the next President (my forecasts also assume a Clinton presidency). The alternative is too grim to contemplate.

Although the race has narrowed, the markets and political aggregators are suggesting the most likely outcome is split government, with Hillary Clinton in the White House and the Republicans in control of the House. This would imply that the gridlock in Washington continues and that policy changes would not be significant – which is assumed in our baseline economic forecasts. However, we cannot rule out the possibility of a Republican sweep. As our strategists have noted, the initial reaction to a potential Trump victory would likely be a risk-off event in the markets, which we think could end up delaying the Fed from hiking in December.

emphasis added

Friday:

• At 8:30 AM ET, Personal Income and Outlays for August. The consensus is for a 0.2% increase in personal income, and for a 0.2% increase in personal spending. And for the Core PCE price index to increase 0.2%.

• At 9:45 AM, Chicago Purchasing Managers Index for September. The consensus is for a reading of 52.0, up from 51.5 in August.

• At 10:00 AM, University of Michigan's Consumer sentiment index (final for September). The consensus is for a reading of 90.1, up from the preliminary reading 89.8.

from Calculated Risk http://ift.tt/2cZUJ6W

via YQ Matrix

China metspar prices drop in September

Lower grade fluorspar products out of China see prices falling for the third consecutive week in the last month; demand from steel and cement remains bleak

from MPW - Pricing News http://ift.tt/2cEOCUo

via IFTTT

from MPW - Pricing News http://ift.tt/2cEOCUo

via IFTTT

Low rare earth prices continue to hurt Lynas

Large production increases of NdPr and rare earth oxides generally were more than countered by weakening prices, causing the company’s net loss to widen by 14% in the 2016 financial year.

from MPW - Pricing News http://ift.tt/2duHOPi

via IFTTT

from MPW - Pricing News http://ift.tt/2duHOPi

via IFTTT

Zillow Forecast: Expect Similar YoY Growth in August for the Case-Shiller Indexes

The Case-Shiller house price indexes for July were released Tuesday. Zillow forecasts Case-Shiller a month early, and I like to check the Zillow forecasts since they have been pretty close.

From Zillow: August Case-Shiller Forecast: New Home Price Peaks Within Sight

from Calculated Risk http://ift.tt/2dHtJgn

via YQ Matrix

From Zillow: August Case-Shiller Forecast: New Home Price Peaks Within Sight

According to Zillow’s August Case-Shiller forecast, the national index and both smaller 10 and 20-city indices look set to keep growing at a very similar rate as they have been for the past few months. After two full years of steady growth around 5 percent annually, the U.S. National Case-Shiller home price index is within striking distance of reaching its July 2006 peak levels, just 0.6 percent off those levels, according to today’s data.The year-over-year change for the 20-city index will probably be slightly lower in the August report than in the July report. The change for the National index will probably be slightly higher.

The August Case-Shiller National Index is expected to grow 5.2 percent year-over-year and 0.5 percent month-to-month (seasonally adjusted). We expect the 10-City Index to grow 4.1 percent year-over-year and to stay flat (SA) from July. The 20-City Index is expected to grow 4.9 percent between August 2015 and August 2016, and rise 0.1 percent (SA) from July.

Zillow’s August Case-Shiller forecast is shown in the table below. These forecasts are based on today’s July Case-Shiller data release and the August 2016 Zillow Home Value Index (ZHVI). The August S&P CoreLogic Case-Shiller Indices will not be officially released until Tuesday, October 25.

from Calculated Risk http://ift.tt/2dHtJgn

via YQ Matrix

Wednesday 28 September 2016

Graphite Juniors News in Brief 28 September

A brief roundup of notable junior activities in the graphite industry.

from MPW - Pricing News http://ift.tt/2daQCIi

via IFTTT

from MPW - Pricing News http://ift.tt/2daQCIi

via IFTTT

OPEC Agrees to Cut Oil Output

From Bloomberg: OPEC Agrees to First Oil Output Cut in Eight Years

Click on graph for larger image

Click on graph for larger image

This graph shows the year-over-year change in WTI based on data from the EIA.

Five times since 1987, oil prices have increased 100% or more YoY. And several times prices have almost fallen in half YoY.

Brent and WTI oil prices are now up about 5% year-over-year.

The second graph shows WTI and Brent spot oil prices from the EIA. (Prices today added).

The second graph shows WTI and Brent spot oil prices from the EIA. (Prices today added).

According to Bloomberg, WTI is at $46.83 per barrel today, and Brent is at $48.41.

Prices really collapsed at the end of 2014 - and then rebounded a little - and then collapsed again at the end of 2015 and in early 2016.

Who knows if this agreement will hold, but it seems likely that oil prices - and eventually gasoline prices - will be up year-over-year at the end of 2016 and no longer a drag on CPI.

from Calculated Risk http://ift.tt/2drZ1sG

via YQ Matrix

In two days of round-the-clock talks in Algiers, the group agreed to drop production to 32.5 million barrels a day, the delegate said, asking not to be named because the decision isn’t yet public. That’s nearly 750,000 barrels a day less than it pumped in August.

...

As OPEC agreed to limit its output, Russia smashed a post-Soviet oil-supply record, pumping 11.1 million barrels a day in September, up 400,000 from August, according to preliminary estimates. Russia participated in the Algiers talks, but it’s not party to the OPEC deal.

This graph shows the year-over-year change in WTI based on data from the EIA.

Five times since 1987, oil prices have increased 100% or more YoY. And several times prices have almost fallen in half YoY.

Brent and WTI oil prices are now up about 5% year-over-year.

According to Bloomberg, WTI is at $46.83 per barrel today, and Brent is at $48.41.

Prices really collapsed at the end of 2014 - and then rebounded a little - and then collapsed again at the end of 2015 and in early 2016.

Who knows if this agreement will hold, but it seems likely that oil prices - and eventually gasoline prices - will be up year-over-year at the end of 2016 and no longer a drag on CPI.

from Calculated Risk http://ift.tt/2drZ1sG

via YQ Matrix

Tuesday 27 September 2016

Real Prices and Price-to-Rent Ratio in July

Here is the earlier post on Case-Shiller: Case-Shiller: National House Price Index increased 5.1% year-over-year in July

The year-over-year increase in prices is mostly moving sideways now around 5%. In July, the index was up 5.1% YoY.

In the earlier post, I graphed nominal house prices, but it is also important to look at prices in real terms (inflation adjusted). Case-Shiller, CoreLogic and others report nominal house prices. As an example, if a house price was $200,000 in January 2000, the price would be close to $275,000 today adjusted for inflation (37%). That is why the second graph below is important - this shows "real" prices (adjusted for inflation).

It has been almost ten years since the bubble peak. In the Case-Shiller release this morning, the National Index was reported as being 2.2% below the bubble peak (seasonally adjusted). However, in real terms, the National index is still about 16.6% below the bubble peak.

Nominal House Prices

The first graph shows the monthly Case-Shiller National Index SA, the monthly Case-Shiller Composite 20 SA, and the CoreLogic House Price Indexes (through June) in nominal terms as reported.

The first graph shows the monthly Case-Shiller National Index SA, the monthly Case-Shiller Composite 20 SA, and the CoreLogic House Price Indexes (through June) in nominal terms as reported.

In nominal terms, the Case-Shiller National index (SA) is back to December 2005 levels, and the Case-Shiller Composite 20 Index (SA) is back to June 2005 levels, and the CoreLogic index (NSA) is back to July 2005.

Real House Prices

The second graph shows the same three indexes in real terms (adjusted for inflation using CPI less Shelter). Note: some people use other inflation measures to adjust for real prices.

The second graph shows the same three indexes in real terms (adjusted for inflation using CPI less Shelter). Note: some people use other inflation measures to adjust for real prices.

CPI less Shelter has declined over the last two years pushing up real house prices.

In real terms, the National index is back to January 2004 levels, the Composite 20 index is back to October 2003, and the CoreLogic index back to November 2003.

In real terms, house prices are back to late 2003 levels.

Price-to-Rent

In October 2004, Fed economist John Krainer and researcher Chishen Wei wrote a Fed letter on price to rent ratios: House Prices and Fundamental Value. Kainer and Wei presented a price-to-rent ratio using the OFHEO house price index and the Owners' Equivalent Rent (OER) from the BLS.

Here is a similar graph using the Case-Shiller National, Composite 20 and CoreLogic House Price Indexes.

Here is a similar graph using the Case-Shiller National, Composite 20 and CoreLogic House Price Indexes.

This graph shows the price to rent ratio (January 1998 = 1.0).

On a price-to-rent basis, the Case-Shiller National index is back to July 2003 levels, the Composite 20 index is back to April 2003 levels, and the CoreLogic index is back to June 2003.

In real terms, and as a price-to-rent ratio, prices are back to late 2003 - and the price-to-rent ratio maybe moving a little more sideways now.

from Calculated Risk http://ift.tt/2cIyLaY

via YQ Matrix

The year-over-year increase in prices is mostly moving sideways now around 5%. In July, the index was up 5.1% YoY.

In the earlier post, I graphed nominal house prices, but it is also important to look at prices in real terms (inflation adjusted). Case-Shiller, CoreLogic and others report nominal house prices. As an example, if a house price was $200,000 in January 2000, the price would be close to $275,000 today adjusted for inflation (37%). That is why the second graph below is important - this shows "real" prices (adjusted for inflation).

It has been almost ten years since the bubble peak. In the Case-Shiller release this morning, the National Index was reported as being 2.2% below the bubble peak (seasonally adjusted). However, in real terms, the National index is still about 16.6% below the bubble peak.

Nominal House Prices

In nominal terms, the Case-Shiller National index (SA) is back to December 2005 levels, and the Case-Shiller Composite 20 Index (SA) is back to June 2005 levels, and the CoreLogic index (NSA) is back to July 2005.

Real House Prices

CPI less Shelter has declined over the last two years pushing up real house prices.

In real terms, the National index is back to January 2004 levels, the Composite 20 index is back to October 2003, and the CoreLogic index back to November 2003.

In real terms, house prices are back to late 2003 levels.

Price-to-Rent

In October 2004, Fed economist John Krainer and researcher Chishen Wei wrote a Fed letter on price to rent ratios: House Prices and Fundamental Value. Kainer and Wei presented a price-to-rent ratio using the OFHEO house price index and the Owners' Equivalent Rent (OER) from the BLS.

This graph shows the price to rent ratio (January 1998 = 1.0).

On a price-to-rent basis, the Case-Shiller National index is back to July 2003 levels, the Composite 20 index is back to April 2003 levels, and the CoreLogic index is back to June 2003.

In real terms, and as a price-to-rent ratio, prices are back to late 2003 - and the price-to-rent ratio maybe moving a little more sideways now.

from Calculated Risk http://ift.tt/2cIyLaY

via YQ Matrix

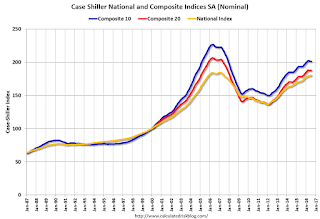

Case-Shiller: National House Price Index increased 5.1% year-over-year in July

S&P/Case-Shiller released the monthly Home Price Indices for July ("July" is a 3 month average of May, June and July prices).

This release includes prices for 20 individual cities, two composite indices (for 10 cities and 20 cities) and the monthly National index.

Note: Case-Shiller reports Not Seasonally Adjusted (NSA), I use the SA data for the graphs.

From S&P: Home Price Gains in July Slow According to the S&P CoreLogic Case-Shiller Indices

Click on graph for larger image.

Click on graph for larger image.

The first graph shows the nominal seasonally adjusted Composite 10, Composite 20 and National indices (the Composite 20 was started in January 2000).

The Composite 10 index is off 11.1% from the peak, and down slightly in July (SA).

The Composite 20 index is off 9.2% from the peak, and down slightly (SA) in July.

The National index is off 2.2% from the peak (SA), and up 0.4% (SA) in July. The National index is up 32.1% from the post-bubble low set in December 2011 (SA).

The second graph shows the Year over year change in all three indices.

The second graph shows the Year over year change in all three indices.

The Composite 10 SA is up 4.2% compared to July 2015.

The Composite 20 SA is up 5.1% year-over-year.

The National index SA is up 5.1% year-over-year.

Note: According to the data, prices increased in 12 of 20 cities month-over-month seasonally adjusted.

I'll have more later.

from Calculated Risk http://ift.tt/2dotk3C

via YQ Matrix

This release includes prices for 20 individual cities, two composite indices (for 10 cities and 20 cities) and the monthly National index.

Note: Case-Shiller reports Not Seasonally Adjusted (NSA), I use the SA data for the graphs.

From S&P: Home Price Gains in July Slow According to the S&P CoreLogic Case-Shiller Indices

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 5.1% annual gain in July, up from 5.0% last month. The 10-City Composite posted a 4.2% annual increase, down from 4.3% the previous month. The 20-City Composite reported a year-over-year gain of 5.0%, down from 5.1% in June.

...

Before seasonal adjustment, the National Index posted a month-over-month gain of 0.7% in July. The 10-City Composite recorded a 0.5% month-over-month increase while the 20-City Composite posted a 0.6% increase in July. After seasonal adjustment, the National Index recorded a 0.4% month-overmonth increase, the 10-City Composite posted a 0.1% decrease, and the 20-City Composite remains unchanged. After seasonal adjustment, 12 cities saw prices rise, two cities were unchanged, and six cities experienced negative monthly prices changes.

emphasis added

The first graph shows the nominal seasonally adjusted Composite 10, Composite 20 and National indices (the Composite 20 was started in January 2000).

The Composite 10 index is off 11.1% from the peak, and down slightly in July (SA).

The Composite 20 index is off 9.2% from the peak, and down slightly (SA) in July.

The National index is off 2.2% from the peak (SA), and up 0.4% (SA) in July. The National index is up 32.1% from the post-bubble low set in December 2011 (SA).

The Composite 10 SA is up 4.2% compared to July 2015.

The Composite 20 SA is up 5.1% year-over-year.

The National index SA is up 5.1% year-over-year.

Note: According to the data, prices increased in 12 of 20 cities month-over-month seasonally adjusted.

I'll have more later.

from Calculated Risk http://ift.tt/2dotk3C

via YQ Matrix

Monday 26 September 2016

Tuesday: Case-Shiller House Prices

Monday Night from 9:00 to 10:30 PM: the First Presidential Debate at Hofstra University in New York.

From Politifact Live fact-checking the first Trump, Clinton presidential debate

From the NY Times: How The New York Times Will Fact-Check the Debate

Tuesday:

• At 9:00 AM ET, S&P/Case-Shiller House Price Index for July. Although this is the July report, it is really a 3 month average of May, June and July prices. The consensus is for a 5.2% year-over-year increase in the Comp 20 index for July. The Zillow forecast is for the National Index to increase 5.0% year-over-year in July.

• At 10:00 AM, Richmond Fed Survey of Manufacturing Activity for September. This is the last of the regional Fed surveys for September.

from Calculated Risk http://ift.tt/2dxGgmG

via YQ Matrix

From Politifact Live fact-checking the first Trump, Clinton presidential debate

From the NY Times: How The New York Times Will Fact-Check the Debate

Tuesday:

• At 9:00 AM ET, S&P/Case-Shiller House Price Index for July. Although this is the July report, it is really a 3 month average of May, June and July prices. The consensus is for a 5.2% year-over-year increase in the Comp 20 index for July. The Zillow forecast is for the National Index to increase 5.0% year-over-year in July.

• At 10:00 AM, Richmond Fed Survey of Manufacturing Activity for September. This is the last of the regional Fed surveys for September.

from Calculated Risk http://ift.tt/2dxGgmG

via YQ Matrix

Black Knight: House Price Index up 0.4% in July, Up 5.3% year-over-year

Note: I follow several house price indexes (Case-Shiller, CoreLogic, Black Knight, Zillow, FHFA, FNC and more). Note: Black Knight uses the current month closings only (not a three month average like Case-Shiller or a weighted average like CoreLogic), excludes short sales and REOs, and is not seasonally adjusted.

From Black Knight: Black Knight Home Price Index Report: July 2016 Transactions, U.S. Home Prices Up 0.4 Percent for the Month; Up 5.3 Percent Year-Over-Year

Note that house prices are close to the bubble peak in nominal terms, but not adjusted for inflation.

from Calculated Risk http://ift.tt/2dvShJb

via YQ Matrix

From Black Knight: Black Knight Home Price Index Report: July 2016 Transactions, U.S. Home Prices Up 0.4 Percent for the Month; Up 5.3 Percent Year-Over-Year

• U.S. home prices were up 0.4 percent for the month, and have gained 5.3 percent from one year agoThe year-over-year increase in this index has been about the same for the last year.

• At $266K, the U.S. HPI has risen over 33 percent from the market’s bottom and is now within just 0.8 percent of a new national peak

• Home prices in nine of the nation’s 20 largest states and 14 of the 40 largest metros hit new peaks in July

Note that house prices are close to the bubble peak in nominal terms, but not adjusted for inflation.

from Calculated Risk http://ift.tt/2dvShJb

via YQ Matrix

Sunday 25 September 2016

Monday: New Home Sales, Presidential Debate

I mentioned this on twitter earlier today:

I spoke to a local infill spec builder yesterday who has been asking me for advice for several years (and happy with my advice!). The builder brought up the election ... The spec builder told me he was thinking of voting for Trump because his tax rate would be lower. I asked him "How is business?"

The spec builder told me 2016 was his best year ever, and the last few years have been the best of his career.

So I asked what he thought would happen if Trump was elected?

We discussed The Wall, more deportations, trade disputes and more. He asked for my advice if Trump is elected: I explained that it is not possible to predict exactly what will happen because Trump's proposals all over the place ... and Congress would probably block some of Trump’s proposals.

But in general, my advice would be to scale back on his spec building.

I also told him that all key forecasters are assuming Ms. Clinton will win, so forecasts will be revised (probably down) ... And if Trump is elected, the changing forecasts would mean the markets will be volatile. He noted that his sales always slow when the markets are volatile.

My conclusion was that voting for a lower tax rate – and probably worse business conditions – seems penny-wise and pound foolish.

Weekend:

• Schedule for Week of Sept 25, 2016

Monday:

• At 10:00 AM ET, New Home Sales for August from the Census Bureau. The consensus is for an decrease in sales to 598 thousand Seasonally Adjusted Annual Rate (SAAR) in August from 654 thousand in July.

• At 10:00 AM, Dallas Fed Survey of Manufacturing Activity for September.

• From 9:00 to 10:30 PM ET: the First Presidential Debate at Hofstra University in New York.

From CNBC: Pre-Market Data and Bloomberg futures: S&P futures are up 1 and DOW futures are up 20 (fair value).

Oil prices were up over the last week with WTI futures at $44.85 per barrel and Brent at $46.26 per barrel. A year ago, WTI was at $45, and Brent was at $47 - so prices are down slightly year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.20 per gallon (down less than $0.10 per gallon from a year ago).

from Calculated Risk http://ift.tt/2dkAK3s

via YQ Matrix

I spoke to a local infill spec builder yesterday who has been asking me for advice for several years (and happy with my advice!). The builder brought up the election ... The spec builder told me he was thinking of voting for Trump because his tax rate would be lower. I asked him "How is business?"

The spec builder told me 2016 was his best year ever, and the last few years have been the best of his career.

So I asked what he thought would happen if Trump was elected?

We discussed The Wall, more deportations, trade disputes and more. He asked for my advice if Trump is elected: I explained that it is not possible to predict exactly what will happen because Trump's proposals all over the place ... and Congress would probably block some of Trump’s proposals.

But in general, my advice would be to scale back on his spec building.

I also told him that all key forecasters are assuming Ms. Clinton will win, so forecasts will be revised (probably down) ... And if Trump is elected, the changing forecasts would mean the markets will be volatile. He noted that his sales always slow when the markets are volatile.

My conclusion was that voting for a lower tax rate – and probably worse business conditions – seems penny-wise and pound foolish.

Weekend:

• Schedule for Week of Sept 25, 2016

Monday:

• At 10:00 AM ET, New Home Sales for August from the Census Bureau. The consensus is for an decrease in sales to 598 thousand Seasonally Adjusted Annual Rate (SAAR) in August from 654 thousand in July.

• At 10:00 AM, Dallas Fed Survey of Manufacturing Activity for September.

• From 9:00 to 10:30 PM ET: the First Presidential Debate at Hofstra University in New York.

From CNBC: Pre-Market Data and Bloomberg futures: S&P futures are up 1 and DOW futures are up 20 (fair value).

Oil prices were up over the last week with WTI futures at $44.85 per barrel and Brent at $46.26 per barrel. A year ago, WTI was at $45, and Brent was at $47 - so prices are down slightly year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.20 per gallon (down less than $0.10 per gallon from a year ago).

from Calculated Risk http://ift.tt/2dkAK3s

via YQ Matrix

Saturday 24 September 2016

Schedule for Week of Sept 25, 2016

The key economic report this week is August New Home Sales. Other key indicators include Personal Income and Outlays for August, and the Case-Shiller House Price Index for July.

Also the third estimate of Q2 GDP will be released.

For manufacturing, the September Richmond and Dallas manufacturing surveys will be released this week.

A key focus will be on the first Presidential debate on Monday.

----- Monday, Sept 26th -----

10:00 AM ET: New Home Sales for August from the Census Bureau.

10:00 AM ET: New Home Sales for August from the Census Bureau.

This graph shows New Home Sales since 1963. The dashed line is the July sales rate.

The consensus is for an decrease in sales to 598 thousand Seasonally Adjusted Annual Rate (SAAR) in August from 654 thousand in July.

10:30 AM: Dallas Fed Survey of Manufacturing Activity for September.

From 9:00 to 10:30 PM: the First Presidential Debate at Hofstra University in New York.

----- Tuesday, Sept 27th -----

9:00 AM ET: S&P/Case-Shiller House Price Index for July. Although this is the July report, it is really a 3 month average of May, June and July prices.

9:00 AM ET: S&P/Case-Shiller House Price Index for July. Although this is the July report, it is really a 3 month average of May, June and July prices.

This graph shows the nominal seasonally adjusted National Index, Composite 10 and Composite 20 indexes through the June 2016 report (the Composite 20 was started in January 2000).

The consensus is for a 5.2% year-over-year increase in the Comp 20 index for July. The Zillow forecast is for the National Index to increase 5.0% year-over-year in July.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for September. This is the last of the regional Fed surveys for September.

----- Wednesday, Sept 28th -----

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: Durable Goods Orders for August from the Census Bureau. The consensus is for a 1.9% decrease in durable goods orders.

10:00 AM: Testimony by Fed Chair Janet Yellen, Supervision and Regulation, Before the Committee on Financial Services, U.S. House of Representatives

----- Thursday, Sept 29th -----

8:30 AM ET: The initial weekly unemployment claims report will be released. The consensus is for 260 thousand initial claims, up from 252 thousand the previous week.

8:30 AM: Gross Domestic Product, 2nd quarter 2016 (Third estimate). The consensus is that real GDP increased 1.3% annualized in Q2, up from 1.1% in the second estimate.

10:00 AM: Pending Home Sales Index for August. The consensus is for a 0.5% increase in the index.

5:10 PM: Speech by Fed Chair Janet Yellen, Conversation with conference participants, At the Banking and the Economy: A Forum for Minority Bankers, Federal Reserve Bank of Kansas City, Kansas City, Missouri

----- Friday, Sept 30th -----

8:30 AM ET: Personal Income and Outlays for August. The consensus is for a 0.2% increase in personal income, and for a 0.2% increase in personal spending. And for the Core PCE price index to increase 0.2%.

9:45 AM: Chicago Purchasing Managers Index for September. The consensus is for a reading of 52.0, up from 51.5 in August.

10:00 AM: University of Michigan's Consumer sentiment index (final for September). The consensus is for a reading of 90.1, up from the preliminary reading 89.8.

from Calculated Risk http://ift.tt/2cZbLU3

via YQ Matrix

Also the third estimate of Q2 GDP will be released.

For manufacturing, the September Richmond and Dallas manufacturing surveys will be released this week.

A key focus will be on the first Presidential debate on Monday.

This graph shows New Home Sales since 1963. The dashed line is the July sales rate.

The consensus is for an decrease in sales to 598 thousand Seasonally Adjusted Annual Rate (SAAR) in August from 654 thousand in July.

10:30 AM: Dallas Fed Survey of Manufacturing Activity for September.

From 9:00 to 10:30 PM: the First Presidential Debate at Hofstra University in New York.

This graph shows the nominal seasonally adjusted National Index, Composite 10 and Composite 20 indexes through the June 2016 report (the Composite 20 was started in January 2000).

The consensus is for a 5.2% year-over-year increase in the Comp 20 index for July. The Zillow forecast is for the National Index to increase 5.0% year-over-year in July.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for September. This is the last of the regional Fed surveys for September.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: Durable Goods Orders for August from the Census Bureau. The consensus is for a 1.9% decrease in durable goods orders.

10:00 AM: Testimony by Fed Chair Janet Yellen, Supervision and Regulation, Before the Committee on Financial Services, U.S. House of Representatives

8:30 AM ET: The initial weekly unemployment claims report will be released. The consensus is for 260 thousand initial claims, up from 252 thousand the previous week.

8:30 AM: Gross Domestic Product, 2nd quarter 2016 (Third estimate). The consensus is that real GDP increased 1.3% annualized in Q2, up from 1.1% in the second estimate.

10:00 AM: Pending Home Sales Index for August. The consensus is for a 0.5% increase in the index.

5:10 PM: Speech by Fed Chair Janet Yellen, Conversation with conference participants, At the Banking and the Economy: A Forum for Minority Bankers, Federal Reserve Bank of Kansas City, Kansas City, Missouri

8:30 AM ET: Personal Income and Outlays for August. The consensus is for a 0.2% increase in personal income, and for a 0.2% increase in personal spending. And for the Core PCE price index to increase 0.2%.

9:45 AM: Chicago Purchasing Managers Index for September. The consensus is for a reading of 52.0, up from 51.5 in August.

10:00 AM: University of Michigan's Consumer sentiment index (final for September). The consensus is for a reading of 90.1, up from the preliminary reading 89.8.

from Calculated Risk http://ift.tt/2cZbLU3

via YQ Matrix

Friday 23 September 2016

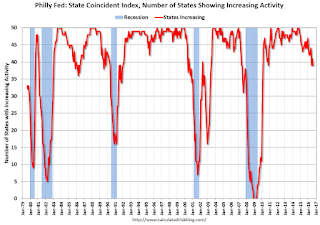

Philly Fed: State Coincident Indexes increased in 39 states in August

From the Philly Fed:

Click on graph for larger image.

Click on graph for larger image.

This is a graph is of the number of states with one month increasing activity according to the Philly Fed. This graph includes states with minor increases (the Philly Fed lists as unchanged).

In August, 39 states had increasing activity.

Six states have seen declines over the last 6 months, in order they are Wyoming (worst), Louisiana, Montana, Kansas, Alaska and Oklahoma - mostly due to the decline in oil prices.

Here is a map of the three month change in the Philly Fed state coincident indicators. This map was all red during the worst of the recession, and is mostly green now.

Here is a map of the three month change in the Philly Fed state coincident indicators. This map was all red during the worst of the recession, and is mostly green now.

Source: Philly Fed. Note: Complaints about red / green issues can be sent to the Philly Fed.

from Calculated Risk http://ift.tt/2d46Mjm

via YQ Matrix

The Federal Reserve Bank of Philadelphia has released the coincident indexes for the 50 states for August 2016. In the past month, the indexes increased in 39 states, decreased in nine, and remained stable in two, for a one-month diffusion index of 60. Over the past three months, the indexes increased in 41 states, decreased in eight, and remained stable in one, for a three month diffusion index of 66.Note: These are coincident indexes constructed from state employment data. An explanation from the Philly Fed:

The coincident indexes combine four state-level indicators to summarize current economic conditions in a single statistic. The four state-level variables in each coincident index are nonfarm payroll employment, average hours worked in manufacturing, the unemployment rate, and wage and salary disbursements deflated by the consumer price index (U.S. city average). The trend for each state’s index is set to the trend of its gross domestic product (GDP), so long-term growth in the state’s index matches long-term growth in its GDP.

This is a graph is of the number of states with one month increasing activity according to the Philly Fed. This graph includes states with minor increases (the Philly Fed lists as unchanged).

In August, 39 states had increasing activity.

Six states have seen declines over the last 6 months, in order they are Wyoming (worst), Louisiana, Montana, Kansas, Alaska and Oklahoma - mostly due to the decline in oil prices.

Source: Philly Fed. Note: Complaints about red / green issues can be sent to the Philly Fed.

from Calculated Risk http://ift.tt/2d46Mjm

via YQ Matrix

IBM invite to join their Futurist Community; Honored to be one of the 50!

I received an invitation from IBM to join their Futurist “think tank” community.

This Community consists of 50 handpicked industry leaders selected based on their field expertise, social presence, and engagement in the Commerce conversation, including supply chain and procurement.

They indicated that they reached out to me because they have been following my coverage of the industry, and view me as a top eCommerce expert and influencer, and among the top 6 in terms of evolving procurement practice.

They are flying me down to Orlando the first week of October – all expenses paid, to participate in a round table discussion with other thought leaders. Needles to say, I am honored and grateful for the opportunity.

I am also excited about being able to connect with other industry thought leaders so that I can add even greater value and expanded insight to the contents of this blog.

Stay tuned.

In the meantime, follow the IBM Futurist Community on Twitter with #NewWaveToEngage

30

from Procurement Insights http://ift.tt/2dpeKI3

This content was assembled for you by the YQ Matrix platform

The views expressed in this post and throughout the series are the autor's own and not intended to reflect the views the YQ Matrix platform, its users or any associated organisations.

For the procurement people among you, have a look at the latest YQ Matrix raw material and semi-finished prices. For: Prices on other websites.

Cheap freight rates make Chinese graphite attractive

Graphite buyers head towards China as low freight costs intensify competition amid weakening downstream demand; flake prices stable at current lows.

from MPW - Pricing News http://ift.tt/2d2JKJm

via IFTTT

from MPW - Pricing News http://ift.tt/2d2JKJm

via IFTTT

Price Briefing 16-22 September

Most minerals' prices remained stable with little trading activities following the mid-autumn festival holiday in China. Imerys has raised its sodium carbonate prices while Orocobre expects its lithium prices to reach $10,000/tonne.

from MPW - Pricing News http://ift.tt/2d5EQgL

via IFTTT

from MPW - Pricing News http://ift.tt/2d5EQgL

via IFTTT

Thursday 22 September 2016

Lawler on August Existing Home Sales

From housing economist Tom Lawler:

In a report released this morning, the National Association of Realtors estimated that US existing home sales ran a seasonally adjusted annual rate of 5.33 million, down 0.9% from July’s downwardly revised (to 5.38 million from 5.39 million) pace and up 0.8% from last August’s seasonally adjusted pace. The NAR’s estimate was well below my above-consensus projection from last week (5.49 million) based on then-available local realtor/MLS reports.

My unusually large “miss” was partly attributable to an under-estimate of the “gap” between the growth in unadjusted home sales compared to seasonally adjusted sales. According to NAR estimates, the YOY growth in unadjusted home sales last month was7.3%, or 6.5 percentage points higher than the YOY increase in seasonally adjusted sales. I had assumed a “gap” of 4.7 percentage points. (This August had two more business days than last August).

In addition, local realtor/MLS reports released since last week (including quite a few released today) showed somewhat lower home sales than I had been assuming for those areas. And finally, even after incorporating local realtor/MLS reports released through today, my “tracking” suggests somewhat faster YOY growth in home sales than that shown by the NAR.

I apologize for my miss this month.

On the inventory front, the NAR estimated that the inventory of existing homes for sale at the end of August totaled 2.04 million, down 3.3% from July and down 10.1% from last August.

Finally, the NAR estimated that the median existing SF home sales price last month was $242.200, up 5.3% from last August.

from Calculated Risk http://ift.tt/2cxiGVr

via YQ Matrix

In a report released this morning, the National Association of Realtors estimated that US existing home sales ran a seasonally adjusted annual rate of 5.33 million, down 0.9% from July’s downwardly revised (to 5.38 million from 5.39 million) pace and up 0.8% from last August’s seasonally adjusted pace. The NAR’s estimate was well below my above-consensus projection from last week (5.49 million) based on then-available local realtor/MLS reports.

My unusually large “miss” was partly attributable to an under-estimate of the “gap” between the growth in unadjusted home sales compared to seasonally adjusted sales. According to NAR estimates, the YOY growth in unadjusted home sales last month was7.3%, or 6.5 percentage points higher than the YOY increase in seasonally adjusted sales. I had assumed a “gap” of 4.7 percentage points. (This August had two more business days than last August).

In addition, local realtor/MLS reports released since last week (including quite a few released today) showed somewhat lower home sales than I had been assuming for those areas. And finally, even after incorporating local realtor/MLS reports released through today, my “tracking” suggests somewhat faster YOY growth in home sales than that shown by the NAR.

I apologize for my miss this month.

On the inventory front, the NAR estimated that the inventory of existing homes for sale at the end of August totaled 2.04 million, down 3.3% from July and down 10.1% from last August.

Finally, the NAR estimated that the median existing SF home sales price last month was $242.200, up 5.3% from last August.

| YOY % Change, Existing Home Sales (NAR Estimate) | ||

|---|---|---|

| Not Seasonally Adjusted | Seasonally Adjusted | |

| July | -6.9% | -1.8% |

| Aug | 7.3% | 0.8% |

| July-August Average | -0.1% | -0.6% |

from Calculated Risk http://ift.tt/2cxiGVr

via YQ Matrix

FHFA: House Price Index Up 0.5 Percent in July

Earlier from the FHFA: FHFA House Price Index Up 0.5 Percent in July 2016

from Calculated Risk http://ift.tt/2dd773T

via YQ Matrix

U.S. house prices rose in July, up 0.5 percent on a seasonally adjusted basis from the previous month, according to the Federal Housing Finance Agency (FHFA) monthly House Price Index (HPI). The previously reported 0.2 percent increase in June was revised upward to reflect a 0.3 percent increase.Most of the other indexes are also showing mid-single digit year-over-year gains.

The FHFA monthly HPI is calculated using home sales price information from mortgages sold to, or guaranteed by, Fannie Mae and Freddie Mac. From July 2015 to July 2016, house prices were up 5.8 percent.

emphasis added

from Calculated Risk http://ift.tt/2dd773T

via YQ Matrix

Kansas City Fed: Regional Manufacturing Activity "Rebounded Moderately" in September

From the Kansas City Fed: Tenth District Manufacturing Activity Rebounded Moderately

from Calculated Risk http://ift.tt/2dkCw4S

via YQ Matrix

The Federal Reserve Bank of Kansas City released the September Manufacturing Survey today. According to Chad Wilkerson, vice president and economist at the Federal Reserve Bank of Kansas City, the survey revealed that Tenth District manufacturing activity increased moderately.The Kansas City region was hit hard by the decline in oil prices, and activity may now be stabilizing.

“For the second time in four months we had a positive reading on our composite index,” said Wilkerson. “This followed 15 straight months of contraction and suggests regional factory activity may be stabilizing.”

...

The month-over-month composite index was 6 in September, up from -4 in August and -6 in July ... The production, shipments, and capital spending indexes were moderately higher, while the employment and order backlog indexes were unchanged. ...

emphasis added

from Calculated Risk http://ift.tt/2dkCw4S

via YQ Matrix

A Few Comments on August Existing Home Sales

Earlier: Existing Home Sales decreased in August to 5.33 million SAAR

Inventory remains a key issue. Here is repeat of two paragraphs I wrote about inventory a few months ago:

I expected some increase in inventory last year, but that didn't happened. Inventory is still very low and falling year-over-year (down 10.1% year-over-year in August). More inventory would probably mean smaller price increases and slightly higher sales, and less inventory means lower sales and somewhat larger price increases.

Two of the key reasons inventory is low: 1) A large number of single family home and condos were converted to rental units. Last year, housing economist Tom Lawler estimated there were 17.5 million renter occupied single family homes in the U.S., up from 10.7 million in 2000. Many of these houses were purchased by investors, and rents have increased substantially, and the investors are not selling (even though prices have increased too). Most of these rental conversions were at the lower end, and that is limiting the supply for first time buyers. 2) Baby boomers are aging in place (people tend to downsize when they are 75 or 80, in another 10 to 20 years for the boomers). Instead we are seeing a surge in home improvement spending, and this is also limiting supply.

Of course low inventory keeps potential move-up buyers from selling too. If someone looks around for another home, and inventory is lean, they may decide to just stay and upgrade.

A key point: Some areas are seeing more inventory. For example, there is more inventory in some coastal areas of California, in New York city and for high rise condos in Miami.

Another key point: I'd consider any existing home sales rate in the 5 to 5.5 million range solid based on the normal historical turnover of the existing stock. As always, it is important to remember that new home sales are more important for jobs and the economy than existing home sales. Since existing sales are existing stock, the only direct contribution to GDP is the broker's commission. There is usually some additional spending with an existing home purchase - new furniture, etc - but overall the economic impact is small compared to a new home sale.

The following graph shows existing home sales Not Seasonally Adjusted (NSA).

Click on graph for larger image.

Click on graph for larger image.

Sales NSA in August (red column) were the highest for August since 2006 (NSA).

Note that sales NSA were strong in August (up 7.3% from August 2015, and up 5.5% from last month), but there were more selling days this year - so the seasonally adjusted number was lower than last month.

from Calculated Risk http://ift.tt/2cFR2Dl

via YQ Matrix

Inventory remains a key issue. Here is repeat of two paragraphs I wrote about inventory a few months ago:

I expected some increase in inventory last year, but that didn't happened. Inventory is still very low and falling year-over-year (down 10.1% year-over-year in August). More inventory would probably mean smaller price increases and slightly higher sales, and less inventory means lower sales and somewhat larger price increases.

Two of the key reasons inventory is low: 1) A large number of single family home and condos were converted to rental units. Last year, housing economist Tom Lawler estimated there were 17.5 million renter occupied single family homes in the U.S., up from 10.7 million in 2000. Many of these houses were purchased by investors, and rents have increased substantially, and the investors are not selling (even though prices have increased too). Most of these rental conversions were at the lower end, and that is limiting the supply for first time buyers. 2) Baby boomers are aging in place (people tend to downsize when they are 75 or 80, in another 10 to 20 years for the boomers). Instead we are seeing a surge in home improvement spending, and this is also limiting supply.

Of course low inventory keeps potential move-up buyers from selling too. If someone looks around for another home, and inventory is lean, they may decide to just stay and upgrade.

A key point: Some areas are seeing more inventory. For example, there is more inventory in some coastal areas of California, in New York city and for high rise condos in Miami.

Another key point: I'd consider any existing home sales rate in the 5 to 5.5 million range solid based on the normal historical turnover of the existing stock. As always, it is important to remember that new home sales are more important for jobs and the economy than existing home sales. Since existing sales are existing stock, the only direct contribution to GDP is the broker's commission. There is usually some additional spending with an existing home purchase - new furniture, etc - but overall the economic impact is small compared to a new home sale.

The following graph shows existing home sales Not Seasonally Adjusted (NSA).

Sales NSA in August (red column) were the highest for August since 2006 (NSA).

Note that sales NSA were strong in August (up 7.3% from August 2015, and up 5.5% from last month), but there were more selling days this year - so the seasonally adjusted number was lower than last month.

from Calculated Risk http://ift.tt/2cFR2Dl

via YQ Matrix

Why I Joined The Revolution

Stand Up. Speak Out. Drive Change.

This is Kelly Barner’s and Philip Ideson’s call to join the revolution . . . the Procurement Revolution.

We are not talking about just a snappy tagline here with a great logo. When Barner and Ideson talk revolution they are using real fighting words. They are talking about the need to reshape our profession and industry in a manner that is revolutionary!

While I will let you check out the Revolution website to get all the details as to how you can add your voice to this important movement, I want to share with you my reasons for joining the Procurement Revolution.

To start, and with a list of over 30 industry notables signing on to share their ideas and visions for a better procurement tomorrow, I believe that this is the first truly collective and coordinated initiative for meaningful change in our profession. It is not an event within the framework of the status quo, but perhaps the beginnings of a seismic shift.

Sure there have been individual or lone voices here and there such as yours truly, who have been willing to speak up in the face of establishment criticism . . . although I still consider being called the Fenimore Cooper of procurement blogs by one industry pundit an honor.

What is even more interesting than the names of those who have joined Kelly and Philip’s revolution, are the names of those which are absent. Could this be an indication that one time industry insiders and perceived thought leaders are now the one’s on the outside looking in? After all, who would not want to be part of such an important discussion?

This of course is the perfect segue into my second reason for joining the revolution . . . no sponsors = no outside influences.

For years the procurement world – and more specifically, the industry’s media, have more often than not, been the paid voice of the service provider community. In other words, the only perspective that was ever really presented, was from a single point of interest.

This doesn’t mean that members of the service provider community are not welcome. It simply means that they will no longer have the sole or dominant voice. This is good for everyone in that through a truly collaborative dialogue, we can all collectively realize our greater aspirations.

In short, it’s time that we procurement professionals take control of the podium of our own futures, and in the process become the definitive voices in our own industry.

Now that’s a R-E-V-O-L-U-T-I-O-N!

30

from Procurement Insights http://ift.tt/2cNFmn8

This content was assembled for you by the YQ Matrix platform

The views expressed in this post and throughout the series are the autor's own and not intended to reflect the views the YQ Matrix platform, its users or any associated organisations.

For the procurement people among you, have a look at the latest YQ Matrix raw material and semi-finished prices. For: Prices on other websites.

Wednesday 21 September 2016

Merrill: "Fed signals December hike"

This is now the consensus view - one rate hike in 2016, most likely in December (but the November meeting is "live") ... From Merrill Lynch: Fed signals December hike

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for 261 thousand initial claims, up from 260 thousand the previous week.

• Also at 8:30 AM, Chicago Fed National Activity Index for August. This is a composite index of other data.

• At 9:00 AM, FHFA House Price Index for July 2016. This was originally a GSE only repeat sales, however there is also an expanded index. The consensus is for a 0.4% month-to-month increase for this index.

• At 10:00 AM, Existing Home Sales for August from the National Association of Realtors (NAR). The consensus is for 5.44 million SAAR, up from 5.39 million in July. Housing economist Tom Lawler expects the NAR to report sales of 5.49 million SAAR in August, up 1.9% from July’s preliminary pace.

from Calculated Risk http://ift.tt/2cn7Vlc

via YQ Matrix

The FOMC clearly signaled a hike before the end of the year in both the language and the dots. The Fed made two important changes to the statement. First, the committee noted that near-term risks to the economic outlook “appear roughly balanced”. This is an important step for the Fed to justify hiking rates at an upcoming meeting and is a page out of the playbook from last year. ...Thursday:

Second, the FOMC noted that “the Committee judges that the case for an increase in the federal funds rate has strengthened but decided, for the time being, to wait for further evidence of further progress toward its objectives.” This is a strong signal that the Fed is planning to hike in an upcoming meeting. It is not explicit calendar guidance, but it is a small step in that direction.

emphasis added

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for 261 thousand initial claims, up from 260 thousand the previous week.

• Also at 8:30 AM, Chicago Fed National Activity Index for August. This is a composite index of other data.

• At 9:00 AM, FHFA House Price Index for July 2016. This was originally a GSE only repeat sales, however there is also an expanded index. The consensus is for a 0.4% month-to-month increase for this index.

• At 10:00 AM, Existing Home Sales for August from the National Association of Realtors (NAR). The consensus is for 5.44 million SAAR, up from 5.39 million in July. Housing economist Tom Lawler expects the NAR to report sales of 5.49 million SAAR in August, up 1.9% from July’s preliminary pace.

from Calculated Risk http://ift.tt/2cn7Vlc

via YQ Matrix

FOMC Statement: No Change to Policy, "The case for an increase in the federal funds rate has strengthened"

Preparing for a rate hike soon ...

FOMC Statement:

from Calculated Risk http://ift.tt/2cRcl7L

via YQ Matrix

FOMC Statement:

Information received since the Federal Open Market Committee met in July indicates that the labor market has continued to strengthen and growth of economic activity has picked up from the modest pace seen in the first half of this year. Although the unemployment rate is little changed in recent months, job gains have been solid, on average. Household spending has been growing strongly but business fixed investment has remained soft. Inflation has continued to run below the Committee's 2 percent longer-run objective, partly reflecting earlier declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation remain low; most survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market conditions will strengthen somewhat further. Inflation is expected to remain low in the near term, in part because of earlier declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of past declines in energy and import prices dissipate and the labor market strengthens further. Near-term risks to the economic outlook appear roughly balanced. The Committee continues to closely monitor inflation indicators and global economic and financial developments.

Against this backdrop, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent. The Committee judges that the case for an increase in the federal funds rate has strengthened but decided, for the time being, to wait for further evidence of continued progress toward its objectives. The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee's holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; James Bullard; Stanley Fischer; Jerome H. Powell; and Daniel K. Tarullo. Voting against the action were: Esther L. George, Loretta J. Mester, and Eric Rosengren, each of whom preferred at this meeting to raise the target range for the federal funds rate to 1/2 to 3/4 percent.

emphasis added

from Calculated Risk http://ift.tt/2cRcl7L

via YQ Matrix

Imerys to increase calcium carbonate price

The hike will take place in December, driven by the rising costs of mining and processing.

from MPW - Pricing News http://ift.tt/2d4mkIs

via IFTTT

from MPW - Pricing News http://ift.tt/2d4mkIs

via IFTTT

Tuesday 20 September 2016

Look Back: In 2006 I predicted House Prices would fall 40%+ in the Bay Area

A reader asked about an old (and I suppose bold at the time) prediction ...

In 2006 I wrote Bay Area: How far will prices fall?

According to Case-Shiller, prices in San Francisco peaked in March 2006 with the index at 219.31. Prices bottomed in San Francisco in May of 2009 at 119.97. That was a nominal decline of 45% (real of 50%), however in a shorter period than I expected - probably because of the boom in tech. Most areas bottomed in early 2012 (the expected 5 to 7 years).

Other areas of the Bay Area probably did worse.

As I noted in 2006, I predicted the price decline based on previous housing busts, and factored in the larger bubble.

But what have I done lately? Nothing bold, unless this counts. I think we can agree those recession calls were incorrect.

from Calculated Risk http://ift.tt/2cB3N1L

via YQ Matrix

In 2006 I wrote Bay Area: How far will prices fall?

In the comments to the previous post I suggested that Bay Area prices might fall 40%+ in real terms over 5 to 7 years. ac asked how I came up with that estimate, and Lester suggested somewhat impolitely that the estimate did not match my "moderate, professorial tone".So how far did prices fall?

According to Case-Shiller, prices in San Francisco peaked in March 2006 with the index at 219.31. Prices bottomed in San Francisco in May of 2009 at 119.97. That was a nominal decline of 45% (real of 50%), however in a shorter period than I expected - probably because of the boom in tech. Most areas bottomed in early 2012 (the expected 5 to 7 years).

Other areas of the Bay Area probably did worse.

As I noted in 2006, I predicted the price decline based on previous housing busts, and factored in the larger bubble.

But what have I done lately? Nothing bold, unless this counts. I think we can agree those recession calls were incorrect.

from Calculated Risk http://ift.tt/2cB3N1L

via YQ Matrix

Monday 19 September 2016

China’s fluorspar prices fall on low demand

Falling demand for acid grade fluorspar has compelled Chinese suppliers to decrease their offers approaching autumn, a period likely to see lower trades amid intense competition, as metspar prices follow suit.

from MPW - Pricing News http://ift.tt/2chYUty

via IFTTT

from MPW - Pricing News http://ift.tt/2chYUty

via IFTTT

Ceramic-grade kaolin prices stable ahead of 2017 contract talks

As the industry gears up for 2017 contract negotiations the price of kaolin from Vietnam continues to hold steady as even some supply disruptions fail to offset the weak demand outlook.

from MPW - Pricing News http://ift.tt/2cCd3YP

via IFTTT

from MPW - Pricing News http://ift.tt/2cCd3YP

via IFTTT

Sunday 18 September 2016

Sunday Night Futures

From James Hamilton at Econbrowser: Why didn’t the recent oil price decline help the U.S. economy more? A few excerpts:

• Schedule for Week of Sept 18, 2016

Monday:

• At 10:00 AM ET, The September NAHB homebuilder survey. The consensus is for a reading of 60, unchanged from 60 in August. Any number above 50 indicates that more builders view sales conditions as good than poor.

From CNBC: Pre-Market Data and Bloomberg futures: S&P futures are up 6 and DOW futures are up 55 (fair value).

Oil prices were down over the last week with WTI futures at $43.67 per barrel and Brent at $46.29 per barrel. A year ago, WTI was at $45, and Brent was at $47 - so prices are down slightly year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.21 per gallon (down about $0.10 per gallon from a year ago).

from Calculated Risk http://ift.tt/2d0uQV9

via YQ Matrix

Baumeister and Kilian update those calculations and conclude that there was a significant boost to consumer spending, noting that real consumption spending grew on average by 3.1% over the two years since oil prices began falling in 2014:Q3 compared with only 2.0% during the preceding two years. ... But gains to consumer spending were mostly offset by a drop in oil-related investment spending.Weekend:

...

Their paper examined a number of details of the economic response. The bottom line is that there seemed to be little net stimulus to the U.S. economy from the collapse in oil prices.

• Schedule for Week of Sept 18, 2016

Monday:

• At 10:00 AM ET, The September NAHB homebuilder survey. The consensus is for a reading of 60, unchanged from 60 in August. Any number above 50 indicates that more builders view sales conditions as good than poor.

From CNBC: Pre-Market Data and Bloomberg futures: S&P futures are up 6 and DOW futures are up 55 (fair value).

Oil prices were down over the last week with WTI futures at $43.67 per barrel and Brent at $46.29 per barrel. A year ago, WTI was at $45, and Brent was at $47 - so prices are down slightly year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.21 per gallon (down about $0.10 per gallon from a year ago).

from Calculated Risk http://ift.tt/2d0uQV9

via YQ Matrix

Saturday 17 September 2016

Schedule for Week of Sept 18, 2016

The key economic reports this week are August housing starts and Existing Home Sales.

The FOMC meets on Tuesday and Wednesday, and no change to policy is expected.

----- Monday, Sept 19th -----

10:00 AM: The September NAHB homebuilder survey. The consensus is for a reading of 60, unchanged from 60 in August. Any number above 50 indicates that more builders view sales conditions as good than poor.

----- Tuesday, Sept 20th -----

8:30 AM: Housing Starts for August.

8:30 AM: Housing Starts for August.

Total housing starts increased to 1.211 million (SAAR) in July. Single family starts increased to 770 thousand SAAR in July.

The consensus for 1.190 million, down from the July rate.

10:00 AM: Regional and State Employment and Unemployment (Monthly) for August 2016

----- Wednesday, Sept 21st -----

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

During the day: The AIA's Architecture Billings Index for August (a leading indicator for commercial real estate).

2:00 PM: FOMC Meeting Announcement. No change to the Fed Funds rate is expected at this meeting.

2:00 PM: FOMC Forecasts This will include the Federal Open Market Committee (FOMC) participants' projections of the appropriate target federal funds rate along with the quarterly economic projections.

2:30 PM: Fed Chair Janet Yellen holds a press briefing following the FOMC announcement.

----- Thursday, Sept 22nd -----

8:30 AM ET: The initial weekly unemployment claims report will be released. The consensus is for 261 thousand initial claims, up from 260 thousand the previous week.

8:30 AM ET: Chicago Fed National Activity Index for August. This is a composite index of other data.

9:00 AM: FHFA House Price Index for July 2016. This was originally a GSE only repeat sales, however there is also an expanded index. The consensus is for a 0.4% month-to-month increase for this index.

10:00 AM: Existing Home Sales for August from the National Association of Realtors (NAR). The consensus is for 5.44 million SAAR, up from 5.39 million in July.

10:00 AM: Existing Home Sales for August from the National Association of Realtors (NAR). The consensus is for 5.44 million SAAR, up from 5.39 million in July.

Housing economist Tom Lawler expects the NAR to report sales of 5.49 million SAAR in August, up 1.9% from July’s preliminary pace.

----- Friday, Sept 23rd -----

No major releases scheduled.

from Calculated Risk http://ift.tt/2d22G04

via YQ Matrix

The FOMC meets on Tuesday and Wednesday, and no change to policy is expected.

10:00 AM: The September NAHB homebuilder survey. The consensus is for a reading of 60, unchanged from 60 in August. Any number above 50 indicates that more builders view sales conditions as good than poor.

Total housing starts increased to 1.211 million (SAAR) in July. Single family starts increased to 770 thousand SAAR in July.

The consensus for 1.190 million, down from the July rate.

10:00 AM: Regional and State Employment and Unemployment (Monthly) for August 2016

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

During the day: The AIA's Architecture Billings Index for August (a leading indicator for commercial real estate).

2:00 PM: FOMC Meeting Announcement. No change to the Fed Funds rate is expected at this meeting.

2:00 PM: FOMC Forecasts This will include the Federal Open Market Committee (FOMC) participants' projections of the appropriate target federal funds rate along with the quarterly economic projections.

2:30 PM: Fed Chair Janet Yellen holds a press briefing following the FOMC announcement.

8:30 AM ET: The initial weekly unemployment claims report will be released. The consensus is for 261 thousand initial claims, up from 260 thousand the previous week.

8:30 AM ET: Chicago Fed National Activity Index for August. This is a composite index of other data.

9:00 AM: FHFA House Price Index for July 2016. This was originally a GSE only repeat sales, however there is also an expanded index. The consensus is for a 0.4% month-to-month increase for this index.

Housing economist Tom Lawler expects the NAR to report sales of 5.49 million SAAR in August, up 1.9% from July’s preliminary pace.

No major releases scheduled.

from Calculated Risk http://ift.tt/2d22G04

via YQ Matrix

Friday 16 September 2016

Lawler: Early Read on Existing Home Sales in August

From housing economist Tom Lawler:

Based on publicly-available state and local realtor/MLS reports from across the country released through today, I project that existing home sales as estimated by the National Association of Realtors ran at a seasonally adjusted annual rate of 5.49 million in August, up 1.9% from July’s preliminary pace and up 3.8% from last August’s seasonally adjusted pace. Unadjusted sales last month should register a significantly larger YOY increase than seasonally adjusted sales, as there were two more business days this August compared to last August.

Local realtor/MLS data also suggest that existing home listings in aggregate declined slightly last month, and I project that the inventory of existing homes for sale as estimated by the NAR for the end of August will be 2.11 million, down 0.9% from July’s preliminary estimate and down 7.0% from last August.. Finally, local realtor/MLS data suggest that the NAR’s estimate of the median existing single-family home sales price for August will be up about 6.3% from last August.

CR Note: The NAR is scheduled to release August existing home sales on Thursday, September 22nd. The consensus is for 5.39 million SAAR in August. Take the over!

from Calculated Risk http://ift.tt/2d6zjsw

via YQ Matrix

Based on publicly-available state and local realtor/MLS reports from across the country released through today, I project that existing home sales as estimated by the National Association of Realtors ran at a seasonally adjusted annual rate of 5.49 million in August, up 1.9% from July’s preliminary pace and up 3.8% from last August’s seasonally adjusted pace. Unadjusted sales last month should register a significantly larger YOY increase than seasonally adjusted sales, as there were two more business days this August compared to last August.

Local realtor/MLS data also suggest that existing home listings in aggregate declined slightly last month, and I project that the inventory of existing homes for sale as estimated by the NAR for the end of August will be 2.11 million, down 0.9% from July’s preliminary estimate and down 7.0% from last August.. Finally, local realtor/MLS data suggest that the NAR’s estimate of the median existing single-family home sales price for August will be up about 6.3% from last August.

CR Note: The NAR is scheduled to release August existing home sales on Thursday, September 22nd. The consensus is for 5.39 million SAAR in August. Take the over!

from Calculated Risk http://ift.tt/2d6zjsw

via YQ Matrix

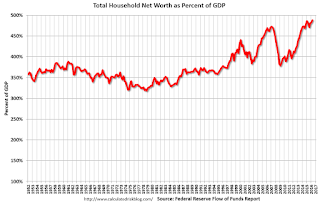

Fed's Flow of Funds: Household Net Worth increased in Q2

The Federal Reserve released the Q2 2016 Flow of Funds report today: Flow of Funds.

According to the Fed, household net worth increased in Q2 compared to Q1:

The Fed estimated that the value of household real estate increased to $22.3 trillion in Q2. The value of household real estate is just below the bubble peak in early 2006 (not adjusted for inflation, and including new construction).

Click on graph for larger image.

Click on graph for larger image.

The first graph shows Households and Nonprofit net worth as a percent of GDP. Household net worth, as a percent of GDP, is higher than the peak in 2006 (housing bubble), and above the stock bubble peak.

This includes real estate and financial assets (stocks, bonds, pension reserves, deposits, etc) net of liabilities (mostly mortgages). Note that this does NOT include public debt obligations.

This graph shows homeowner percent equity since 1952.

This graph shows homeowner percent equity since 1952.

Household percent equity (as measured by the Fed) collapsed when house prices fell sharply in 2007 and 2008.

In Q2 2016, household percent equity (of household real estate) was at 57.1% - up from Q1, and the highest since Q2 2006. This was because of an increase in house prices in Q2 (the Fed uses CoreLogic).

Note: about 30.3% of owner occupied households had no mortgage debt as of April 2010. So the approximately 50+ million households with mortgages have far less than 57.1% equity - and a few million homeowners still have negative equity.

The third graph shows household real estate assets and mortgage debt as a percent of GDP.

The third graph shows household real estate assets and mortgage debt as a percent of GDP.

Mortgage debt increased by $56 billion in Q2.

Mortgage debt has declined by $1.27 trillion from the peak. Studies suggest most of the decline in debt has been because of foreclosures (or short sales), but some of the decline is from homeowners paying down debt (sometimes so they can refinance at better rates).

The value of real estate, as a percent of GDP, was up in Q2, and is above the average of the last 30 years (excluding bubble).

from Calculated Risk http://ift.tt/2csH1cC

via YQ Matrix

According to the Fed, household net worth increased in Q2 compared to Q1:

The net worth of households and nonprofits rose to $89.1 trillion during the second quarter of 2016. The value of directly and indirectly held corporate equities increased $452 billion and the value of real estate increased $474 billion.Household net worth was at $89.1 trillion in Q2 2016, up from $88.0 trillion in Q1 2016.

The Fed estimated that the value of household real estate increased to $22.3 trillion in Q2. The value of household real estate is just below the bubble peak in early 2006 (not adjusted for inflation, and including new construction).

The first graph shows Households and Nonprofit net worth as a percent of GDP. Household net worth, as a percent of GDP, is higher than the peak in 2006 (housing bubble), and above the stock bubble peak.

This includes real estate and financial assets (stocks, bonds, pension reserves, deposits, etc) net of liabilities (mostly mortgages). Note that this does NOT include public debt obligations.

Household percent equity (as measured by the Fed) collapsed when house prices fell sharply in 2007 and 2008.

In Q2 2016, household percent equity (of household real estate) was at 57.1% - up from Q1, and the highest since Q2 2006. This was because of an increase in house prices in Q2 (the Fed uses CoreLogic).

Note: about 30.3% of owner occupied households had no mortgage debt as of April 2010. So the approximately 50+ million households with mortgages have far less than 57.1% equity - and a few million homeowners still have negative equity.

Mortgage debt increased by $56 billion in Q2.

Mortgage debt has declined by $1.27 trillion from the peak. Studies suggest most of the decline in debt has been because of foreclosures (or short sales), but some of the decline is from homeowners paying down debt (sometimes so they can refinance at better rates).

The value of real estate, as a percent of GDP, was up in Q2, and is above the average of the last 30 years (excluding bubble).

from Calculated Risk http://ift.tt/2csH1cC

via YQ Matrix

Key Measures Show Inflation close to 2% in August

The Cleveland Fed released the median CPI and the trimmed-mean CPI this morning:

Click on graph for larger image.

Click on graph for larger image.

This graph shows the year-over-year change for these four key measures of inflation. On a year-over-year basis, the median CPI rose 2.6%, the trimmed-mean CPI rose 2.1%, and the CPI less food and energy also rose 2.3%. Core PCE is for June and increased 1.6% year-over-year.

On a monthly basis, median CPI was at 2.8% annualized, trimmed-mean CPI was at 2.6% annualized, and core CPI was at 3.1% annualized.

Using these measures, inflation has generally been moving up, and most of these measures are at or above the Fed's target (Core PCE is still below).

from Calculated Risk http://ift.tt/2cORf8J

via YQ Matrix